Western Hemisphere and U.S. Co-Production Chain Post Significant Uptick in Two-Way Trade

The Western Hemisphere marked a significant uptick in trade in the first half of 2021, driving a 50 percent surge in U.S. apparel imports, as business rebounded following sizable decreases in textile output and trade due to the COVID-19 pandemic last year.

The trends in the latest U.S. government data show that two-way trade between the U.S. and the region is rebounding strongly, as consumer demand for textile products continues to grow. Additionally, global sourcing shifts and pressure on China forced retailers and brands to continue diversifying and consider nearshoring more production to take advantage of the benefits of our free trade agreements (FTAs) in the region.

Please note that the government trade data for the first half of 2021 provides a comparison to the first half of 2020, a year that is considered an anomaly due to the impact of the pandemic. However, the latest data indicates that trade is on track to match and/or exceed 2019 trade figures.

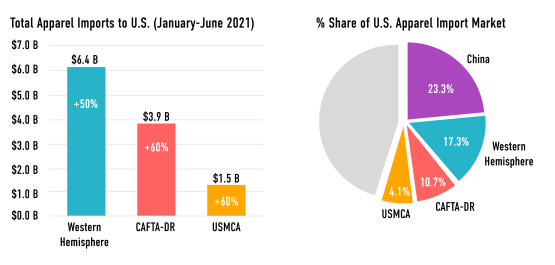

For the year to date through June, apparel imports from the Western Hemisphere (largely comprised of U.S. textile components) jumped 50 percent to $6.4 billion compared with the same period in 2020, according to new data from the Commerce Department’s Office of Textiles and Apparel (OTEXA).

On a year-ending basis through June, the Western Hemisphere controlled a 17.4 percent share of the U.S. apparel import market, an increase of 7.4 percent.

On a year-ending basis through June, the Western Hemisphere controlled a 17.4 percent share of the U.S. apparel import market, an increase of 7.4 percent.

While the rebound is in large part a function of the market bouncing back from the adverse impacts of the COVID-19 pandemic, it is also a reflection of larger sourcing shifts occurring as brands and retailers continue to diversify out of China, which is facing pressures on several fronts.

Most notably, the trade data indicates that China is likely feeling the impact of the imposition of 301 tariffs on the majority of finished Chinese apparel imports, as well as the recent U.S. ban on cotton products from the Xinjiang region of China, following widespread reports of the egregious abuse of Uyghur Muslims and other ethnic minorities and the use of forced labor to produce consumer goods for Western brands.

While apparel and textile imports from China also rose in the first half of the year, the country lost import market share in the U.S.

For the year ending June 30, China had a 23.3 percent share of the U.S. apparel import market, a decline of 13.8% compared to the year-ago period. Its U.S. import share of total textiles and apparel stood at 28%, a decline of 2.8 percent.

A diversification in global sourcing trends has contributed to nearshoring and an increase in orders for Western Hemisphere trading partners.

These positive trends are extremely important for the U.S. textile industry, which has invested heavily in the region and has seen its exports to the region increase significantly, especially under two critical free trade agreements–the U.S. Mexico-Canada-Agreement (USCMA) and the Central America Free Trade Agreement-Dominican Republic (CAFTA-DR).

“The U.S. trade data indicates a strong rebound in the Western Hemisphere, which is gaining U.S. import market share,” said NCTO President and CEO Kim Glas. “I expect this trend to continue through the remainder of this year as retailers and brands seek to nearshore more of their production.

Built on the strength of reciprocal, negotiated FTAs, the Western Hemisphere’s textile supply chain is a vital economic driver for the whole region. Fiber, yarn, and fabric products, and their various associated textile and apparel related end-products, support almost $35 billion in annual two-way trade and more than 2 million direct jobs throughout the hemisphere,” she noted.

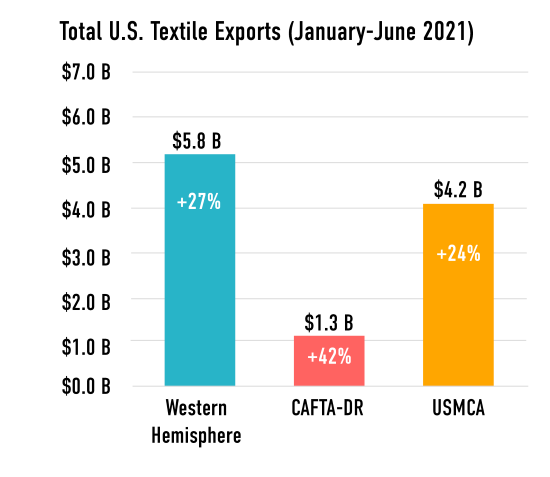

Textile mill product exports to the Western Hemisphere rose 27 percent to $5.8 billion for the year to date, compared to a year ago, while exports to the CAFTA-DR countries rose 42 percent and exports to the USCMA countries increased 24%.

On a more granular level, U.S. yarn exports alone to CAFTA-DR jumped 70 percent year over year, while U.S. fabric exports to USMCA increased 29 percent.

Five of the six CAFTA-DR countries posted double-digit increases in apparel imports in the first half of the year, compared with the first half of 2020,

including: Honduras, with a 78 percent increase to $1.2 billion; El Salvador, an 85 percent increase to $850 million; Guatemala, a 40 percent increase to $753 million, the Dominican Republic, a 52 percent increase to $251 million; and Nicaragua, a 43 percent increase to $864 million.

Total textile and apparel imports from Mexico rose 31.36 percent to $2 billion, while imports from Canada rose 15 percent to $522 million.

Based on the upward trend in imports from the Western Hemisphere, Glas said she is optimistic about the future of the co-production chain in the Western Hemisphere.

She attributed the strength of the partnership to the reciprocal FTAs in the region. “A yarn forward rule in both CAFTA-DR and USMCA ensures that the benefits of the FTA are reserved for manufacturers who actually produce textiles and apparel in the FTA region, as well as strong labor and environmental obligations and commitments embedded in the agreement,” she said.

“We are on track to hit and potentially surpass the two-way trade flows with the Western Hemisphere that we saw in 2019—before the pandemic hit,” Glas said. “We will continue to press this administration and our allies in Congress to maintain policies that allow this co-production chain to flourish.”